Recommendations for action

For consulting services, taking into account sustainability factors contained in the MiFID II-related delegated legislation entails a considerable implementation effort and a risk that should not be underestimated. Among other things, it means extensions to investment advisory and portfolio management systems, comprehensive staff training and revised sales strategies. It is, therefore, essential for affected stakeholders to take action at an early stage to prepare adequately for the requirements.

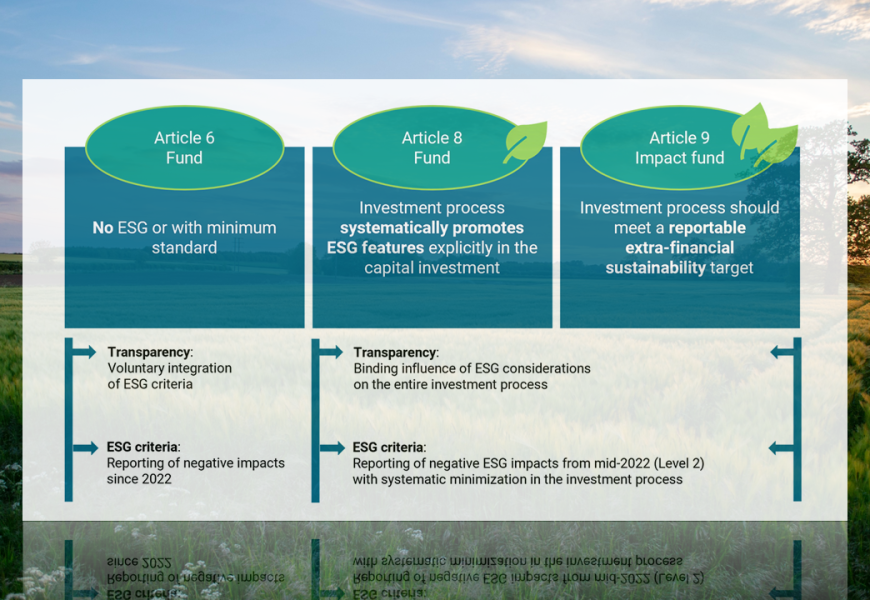

Specifically, it is advisable not only to analyze the existing regulations concerning governance and processes to identify a possible need for adaptation but also to anticipate possible implications for the next technical implementations. This is because, once the SFDR Level II Regulatory Technical Standards (RTS) come into force, fund companies and asset manager will not only have to disclose which of the key negative sustainability impacts (PAIs) of their investments they take into account, but also how they intend to do so and deal with the negative impacts (or justify non-disclosure, if applicable). In addition, they will have to complete comprehensive pre-contractual and periodic disclosure templates or reports, quantitatively and qualitatively, for all funds with environmental and social characteristics (Article 8 funds) and funds with sustainable investment objectives (Article 9 funds).

Torsten Reischmann, Executive Director Product Management Portfolio & Advisory Solutions at Infront

“In the meantime, we have implemented disclosure regulation reports for Article 8 products in particular for our clients and will also provide a standard template as a basis for specific individualisation from mid-May. Due to the lack of clear options for assigning Article 8 products in particular to MIFID sustainability categories, we are currently assuming that we will make adjustments to profiling as well as target market and suitability checks in the first step and then focus on the core regulatory aspects using the German association target market concept. Of course, we will also watch the further interpretations of the associations, such as the VuV and DSGV, and incorporate these into our planned development. We can already support further requirements of individual customers at any time using the individualisation layer of our systems,” says Torsten Reischmann, Executive Director Product Management Portfolio & Advisory Solutions, Infront.